Dixon Technologies Shares Jump 2.67% in Early Trade on Strategic Acquisition News

Dixon Technologies is making headlines again. Its stock jumped 2.67% in early trade thanks to some big news. The company has just announced a new strategic acquisition, and the market has responded positively.

We’ve seen Dixon grow fast in recent years. From assembling LED TVs to making smartphones for top brands, they’ve become a major player in India’s electronics manufacturing space. Now, this latest deal could push them even further.

Advertisement

But what exactly is this acquisition? Why did it cause such a buzz in the market? And what does it mean for investors like us?

In this article, we break down the full story of how Dixon reached this point, what the acquisition is all about, and what experts think about it. Whether you’re an investor, a student, or just curious about the Indian stock market, this is a story worth following.

About Dixon Technologies

We know Dixon Technologies as a fast‑growing electronics contract manufacturer in India. Founded in 1993 by Sunil Vachani, the company operates 17 manufacturing units nationwide, mainly in Noida and Tirupati. They assemble everything from LED TVs and washing machines to smartphones and lighting products.

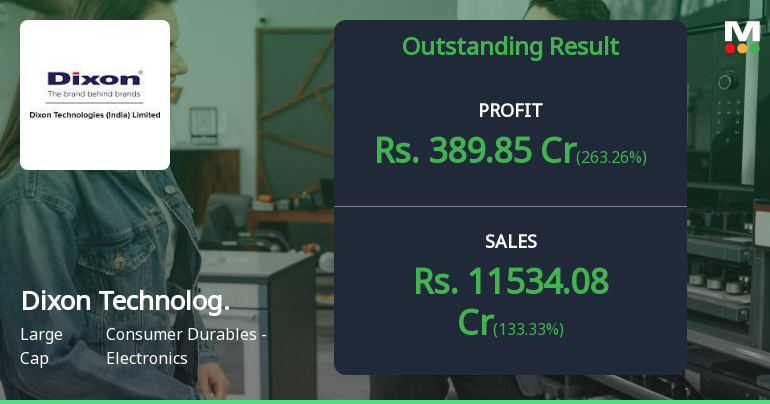

Big brands like Samsung, Xiaomi, Motorola, and Google have used Dixon’s plants to meet their “Make in India” needs. In FY25, Dixon reported revenue of about ₹38,860 crore and a net profit near ₹1,215 crore, showing a strong jump from the previous year.

We’ve seen them move beyond simple assembly into making critical parts, and this latest move builds on that trajectory.

Details of the Strategic Acquisition

On July 15, 2025, Dixon signed a binding term sheet to buy a 51% stake in Kunshan Q Tech Microelectronics (India) through primary and secondary investments. Q Tech India is part of a group that makes camera and fingerprint modules used in phones, IoT devices, and cars. Dixon did not share the deal’s value. The acquisition awaits final approvals and agreement signings.

Strategic Rationale

This deal serves two goals. First, it deepens Dixon’s backward integration. That means making valuable parts in-house. Second, it gives Dixon access to Q Tech’s tech, precision plants, and skilled workforce. Atul Lall, Dixon’s MD, said this is a big step toward building camera and fingerprint modules and improving their supply chain strength.

Market Reaction

The stock market reacted swiftly. Dixon’s shares climbed around 2.6%-4%, touching intraday highs near ₹16,450 before settling about 2.7% higher on July 16. CLSA issued a “High Conviction Outperform” rating, with an ₹15,800 target, and noted the acquisition aligns with Dixon’s move into higher‑value areas.

Meanwhile, Nomura estimated a potential 29% upside and predicted the deal might boost Dixon’s EPS by over 5% by FY28. Trading volumes spiked more than double the usual, suggesting strong investor interest.

Potential Impact on Dixon Technologies

Short-term: We expect revenue and margins to see a positive lift. Q Tech India had ₹2,400 crore in sales with a 5.8% EBITDA margin in FY24. Adding Dixon’s scale, this integration should bolster earnings.

Long-term: The move significantly strengthens Dixon’s hold in smartphone component manufacturing. Nomura predicts that the firm could expand from making 8-10% of a smartphone’s bill of materials to potentially 30% by FY28. That deepens customer partnerships and reduces costs. The acquisition positions Dixon better to serve markets in automotive, IoT, and smart devices.

Risks: The main challenges are integrating a new business and securing approvals. Also, high valuations might make investors cautious, even with strong growth trends.

Industry Implications

This strategic leap speaks volumes about India’s EMS sector. Dixon is answering a growing demand for value‑added components in domestic supply chains. The joint venture with Chongqing Yuhai to make precision mechanical parts is another sign of this intention. Global OEMs operating in India, supported by Production Linked Incentive (PLI) schemes, will likely welcome more such moves.

Competitors like Bharat FIH and Amber Enterprises may feel pressure to stage similar integrations. The broader electronics ecosystem stands to gain from higher local production of sophisticated components.

Analyst Insights and Professional Opinions

Analysts see this as a turning point:

CLSA called it a “High Conviction Outperform,” citing the strategic move into high-value smartphone parts.

Nomura, which maintained a ‘Buy’ rating, thinks Dixon’s leap into components could be worth as much as 29% upside by FY28.

JP Morgan and other brokers also expect earnings upgrades due to tighter integration in the supply chain.

Wrap Up

We’ve seen how Dixon’s decision to acquire a majority stake in Q Tech India is more than another deal. It marks a shift as the company moves from being mainly an assembly partner to becoming a maker of core smartphone components. The market cheered this plan, boosting stock prices and gaining analyst support.

Risks remain like regulatory approvals and integration execution, but we believe this development sets Dixon on a path for higher value, deeper customer ties, and stronger margins. That’s why forward‑looking investors and industry watchers should keep a close eye on Dixon’s next steps.

Advertisement

Frequently Asked Questions (FAQs)

Dixon’s shares rose due to its strategic acquisition of a 51% stake in Q Tech India. Investors expect stronger earnings and higher manufacturing scope.

Analysts have a long-term target around ₹16,800 with a high range near ₹21,400. Some even forecast up to ₹22,000-₹47,000 in the coming years.

Many brokers rate Dixon a long-term buy, citing strong revenue and profit growth, P/E justified by market tailwinds. WalletInvestor sees multi-year upside.

Shares fall when quarterly performance underwhelms or valuations seem high. Also, PLI scheme expiry and profit-booking cause occasional declines.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)