In March 2026, the U.S. mortgage world crossed a major milestone. Fannie Mae, the giant that backs roughly half of all American home loans, announced it will accept crypto‑backed mortgages for the first time. Buyers can now pledge digital assets like Bitcoin or USDC toward a home purchase without selling and triggering taxes.

This clear shift could change how crypto holders finance homes. Instead of cashing out their digital wealth, they may keep it invested while using it to qualify for a mortgage. The move marks a rare moment where cryptocurrency steps out of speculative markets and into everyday financial life.

What Changed, Fannie Mae’s New Crypto Mortgage Rules

The Policy Shift Explained

In March 2026, Fannie Mae signaled a major change in the U.S. mortgage market by formally allowing crypto‑backed mortgage products for the first time. This shift follows a regulatory push in June 2025, when the Federal Housing Finance Agency (FHFA) ordered Fannie Mae and Freddie Mac to prepare to consider cryptocurrency holdings as mortgage assets without converting them to U.S. dollars. This marked a turning point in how digital assets could be used in traditional home financing.

What Cryptocurrencies Qualify?

Under the new structure, homebuyers can pledge digital assets such as Bitcoin (BTC) or the USDC stablecoin as collateral rather than selling them and realizing a taxable event. The actual financing involves two linked loans: a standard mortgage backed by Fannie Mae and a second loan secured by crypto that covers the down payment. This product is being offered via a partnership between Coinbase and mortgage lender Better Home & Finance, with Fannie Mae acting as the guarantor for the primary mortgage.

While Fannie Mae doesn’t originate loans itself, its backing gives this product a level of legitimacy and scale previously unseen in the crypto mortgage space. Importantly, there are no margin calls if the value of the pledged crypto falls, provided the borrower continues to make mortgage payments. This protects homeowners from forced liquidations during downturns in crypto markets.

How the Crypto Down Payment Structure Works?

Instead of requiring borrowers to convert crypto to fiat for a down payment, this new setup lets crypto holders leverage their digital assets directly. The key features include:

- Dual‑loan structure: One traditional mortgage, backed by Fannie Mae. A second loan, backed by crypto, funds the down payment.

- Collateral without margin calls: As long as mortgage payments stay current, crypto value swings do not force extra collateral.

- Asset retention: Borrowers retain exposure to potential crypto gains instead of triggering capital gains taxes by selling.

This approach makes digital assets more functional in everyday finance. It allows homeowners who hold significant crypto to keep their investment intact while still accessing traditional home financing. However, this structure also introduces complexity, as borrowers must manage two concurrent loans and understand how collateral valuation influences borrowing power.

Market Trends, and Data for Crypto Mortgages

Who Benefits Most?

Crypto‑backed mortgages are expected to appeal first to buyers who:

- Hold substantial digital assets but limited cash savings.

- Want to avoid selling crypto and incurring taxes.

- Seek alternative ways to qualify for home loans when traditional cash reserves are limited.

About 14% of Americans owned cryptocurrency in 2025, and a notable share of younger homebuyers have used crypto in down payments by selling holdings. The new structure could shift this dynamic by letting buyers leverage assets without selling.

Mortgage Market Context

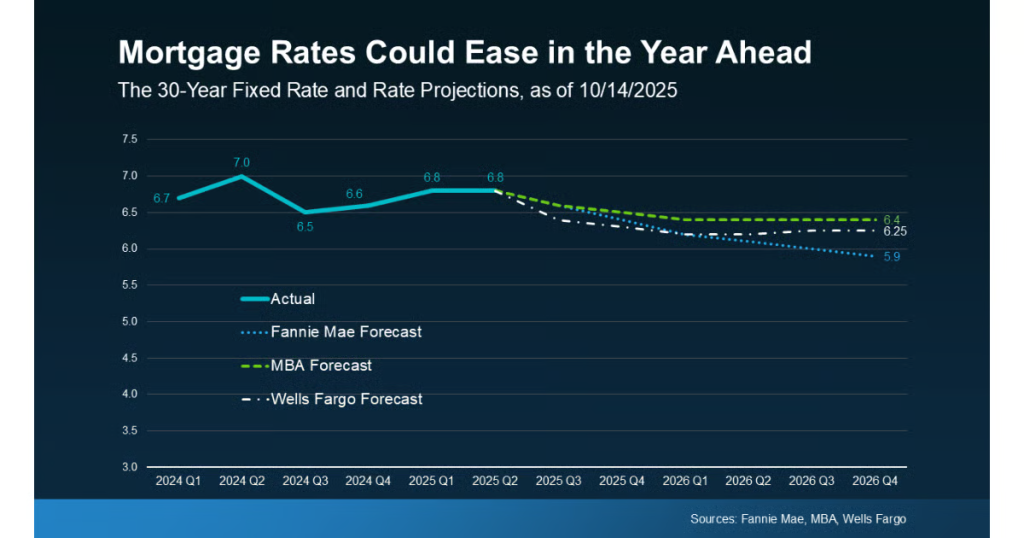

Interest rates and home prices have remained relatively high in early 2026. According to Fannie Mae’s February 2026 housing forecast, the average 30‑year fixed mortgage rate was near 6.0%, and single‑family mortgage originations showed modest gains year‑over‑year in some categories.

In this context, a crypto‑backed down payment could make homeownership more accessible for some buyers. However, lenders may charge a premium, often 0.5 to 1.5 percentage points higher than standard mortgages, to account for added complexity and risk.

Risks, Challenges, and Regulatory Considerations

What are the Main Risks?

Despite the clear benefits, there are several risks and hurdles:

- Volatility: Cryptocurrencies are known for sharp price swings. Even though margin calls are not part of the product, volatility can still affect how lenders value collateral.

- Regulatory uncertainty: While FHFA’s directive shifted policy, implementation details are still evolving. Not all mortgage lenders have fully adapted their processes to accept crypto as qualifying assets.

- Custody requirements: Crypto must typically remain on a regulated exchange or custodian, which may deter users who prefer self‑custody.

Fannie Mae: What Does Regulation Say?

The decision to treat crypto holdings as mortgage assets stems from a June 25, 2025, FHFA directive requiring Fannie Mae and Freddie Mac to prepare proposals to count cryptocurrency toward loan risk assessments without forcing conversion to fiat. Only assets stored on US‑regulated exchanges and verifiable through legal documentation qualify under the directive.

This policy aligns with broader efforts to integrate digital assets into mainstream financial infrastructure. However, final underwriting standards and implementation rules are still being refined as lenders adjust to this new paradigm.

Conclusion

The launch of crypto‑backed mortgage products backed by Fannie Mae represents a major step in blending digital assets with everyday finance. It gives crypto holders a new tool to access traditional homeownership while preserving their investments.

Still, complexity, volatility, and evolving regulations mean this will begin as a niche option. Whether this innovation becomes mainstream will depend on how lenders adapt and how homebuyers respond to the risks and rewards of merging crypto with real estate finance.

Frequently Asked Questions (FAQs)

Yes. As of March 2026, Fannie Mae allows Bitcoin or USDC to be used as mortgage collateral.

Borrowers pledge crypto like Bitcoin or USDC to cover down payments. They keep ownership while securing a home loan.

Crypto value can drop. Even with no margin calls, volatility may affect borrower confidence and lender evaluation in 2026.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)