Costco Stock Maintains Outperform Rating Following Robust June Sales and Warehouse Growth

Costco stock is on a winning streak. In June 2025, the company reported strong sales and opened several new warehouses. That’s big news in the retail world. While some stores struggle to grow, Costco is quietly expanding and keeping its customers happy.

We all know Costco for its bulk items, great prices, and free food samples. But behind the scenes, it’s a retail giant with smart strategies. Its membership model brings in steady revenue.

Its product mix keeps prices low and shoppers loyal. And now, analysts are giving its stock an “Outperform” rating. That means they expect it to do better than most others in the market.

So, why is Costco doing so well right now? What does this rating mean for investors? And how does warehouse growth fit into the big picture? Let’s break it down.

Costco’s June Performance Highlights

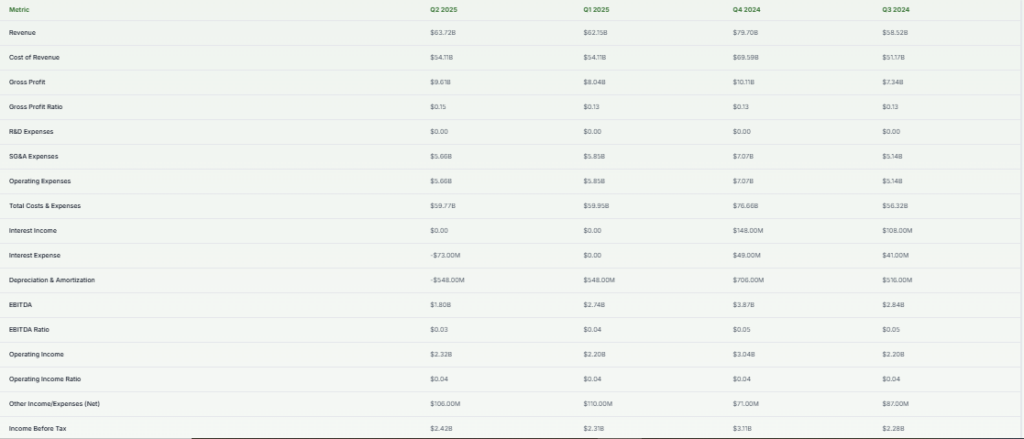

Costco posted $26.44 billion in net sales for June, an 8.0% jump year over year. That beat analysts’ expectations.

Total comparable sales grew 5.8% across the company. In the U.S., comps rose 4.7%, Canada saw 6.7%, and other international markets surged 10.9%.

If you strip out gas price changes and currency swings, the growth looks even better: comps rose 6.2% globally. U.S. comps climbed 5.5%, Canada up 7.9%, and international markets around 8.2%.

E‑commerce was a star performer. Online sales jumped 11.5% year over year. Adjusted for currency effects, the gain was 11.2%.

This June included holiday shopping around Father’s Day, Juneteenth, and Independence Day. It helped fuel demand for barbecue food, candy, meats, and fresh produce.

Warehouse Expansion Strategy

Costco added 25 new warehouses by early Q3. That boosted unit growth by 2.8%. For fiscal 2025, the company plans a total of 27 new openings, of which 24 are net new, pushing its global count to 914 locations.

In spring 2025 saw six new U.S. warehouses were opened across states like California, Texas, Michigan, and Massachusetts. One site in Pleasanton, CA, hit record‑high opening day sales of $2.9 million.

These new locations relieve pressure on crowded stores. They improve parking, reduce checkout wait times, and enhance shopping comfort.

Analyst Rating & Market Response

Several analysts reaffirmed a strong outlook for COST stock. Bernstein reiterated its Outperform rating and a $1,153 price target. They cited strength in the Kirkland Signature brand and consistent growth.

Other firms also agree. UBS grouped Costco with O’Reilly and Walmart as part of a solid retail cluster dubbed “COW.” They see these firms as resilient in uncertain economic times. UBS maintains a Buy rating on Costco.

Oppenheimer analysts also stayed positive. They described Costco as a leader in market share gains. They advised investors to add on dips.

Still, not all are enthusiastic. Roth’s Bill Kirk warned that Costco’s high valuation leaves little room for error if growth slows.

Mizuho remains cautious with a Neutral rating, noting steady U.S. comps and a valuation risk.

Financial Health and Earnings Outlook

Sales growth has been consistent. Costco recently reported a trailing twelve‑month revenue rate of 5.9%, in line with long‑term trends.

Membership fees stay strong. As of fiscal Q3 2025, paid households rose to 79.6 million, and Executive membership grew by 9%, making up nearly 47% of the total. These tiers drive much of Costco’s profit.

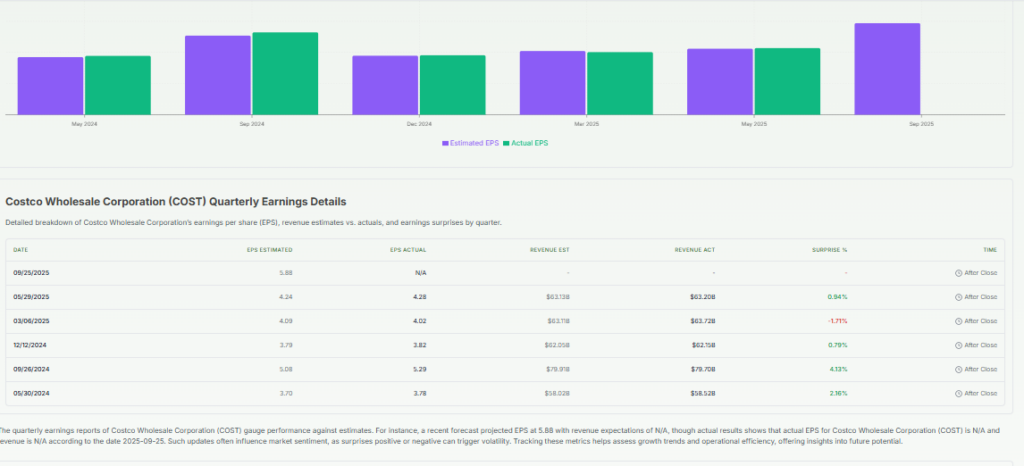

Analysts expect EPS growth of about 10% per year. For fiscal 2025 and 2026, estimates sit around $17.97 and $19.93 per share.

While comps rebounded, valuation remains high. COST trades at about 49-51 times forward earnings, far above broader market levels. Bernstein argues the premium fits Costco’s strong value proposition and margin discipline.

Costco vs. Other Retail Giants

Costco holds an edge over rivals like Sam’s Club, Walmart, and Target. Its bulk pricing, high member renewal, and Kirkland Signature private label ensure loyalty.

In comparison, loyal shoppers return for Costco’s food deals, fuel savings, and seasonal bargains. Competitors struggle to match Costco’s mix of value and exclusivity.

Unique Value Proposition

Kirkland is central to Costco’s strength. Bernstein noted that this private‑label brand matches national brands in quality but sells at roughly 20% below. It now ranks as one of the most recognized private labels in the U.S.

Costco also shifts more sourcing locally. That helps offset tariffs and keeps costs down. For example, Chinese imports are now only 8% of U.S. sales. This helps with pricing stability.

The recent partnership with Affirm provides a buy‑now‑pay‑later option for purchases from $500 to $17,500. It adds flexibility and boosts confidence in buying higher‑ticket items.

Costco Stock: Risks and Challenges

Despite the strong showing, there are headwinds. Inflation pressure, rising labor costs, and supply chain shifts could erode margins.

Currency swings and tariffs may pose risks abroad. Economic slowdowns in key markets could hit demand.

The high valuation means any slowdown may lead to sharp declines in stock price. Bernstein and other cautious voices warn of this risk.

Wrap Up

June’s sales surge and the rollout of new warehouses show Costco executing well. E‑commerce is strong. Comp growth is back. Expansion is steady. Analysts sticking with an Outperform rating underline confidence in the company’s model.

Still, the lofty valuation raises caution. For long‑term investors, Costco offers stability and consistent growth. But for value seekers, it may require patience until a pullback.

Frequently Asked Questions (FAQ)

Costco’s stock has a strong rating from many analysts. Most rate it as “Outperform” or “Buy,” which means they expect it to do better than average stocks.

The retail warehouse industry grows slowly but steadily. Costco’s yearly sales have been growing around 6% to 8%, showing stable progress compared to other stores.

Costco is known for steady growth and loyal shoppers. It may be a good choice for long-term investors, but the high stock price needs careful thinking.

Over the past 5 years, Costco’s stock has returned about 130% total. This shows strong performance, but past success doesn’t guarantee future returns.

Disclaimer:

This is for information only, not financial advice. Always do your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)