The Commonwealth Bank has taken swift action following the Reserve Bank of Australia’s (RBA) latest move, cutting its home loan interest rates to provide relief for homeowners. This comes after the RBA decided to lower the cash rate to 3.60 per cent, the third rate cut of the year, as inflation slows and economic growth cools.

For many Australians juggling rising living costs, this is welcome news. But what exactly does this mean for borrowers, and how will it impact the housing market?

Advertisement

Why did the RBA cut rates now?

The RBA reduced the official cash rate by 0.25 percentage points on August 12, 2025. Governor Michele Bullock cited easing inflation pressures, which are now trending within the RBA’s 2–3 per cent target band, and signs of a softer labour market as key reasons for the decision.

Lower rates are designed to help households manage repayments and to stimulate the economy by encouraging spending and investment. But the real benefit depends on whether banks pass the savings on to customers.

The RBA’s decision to lower the cash rate for the third time this year follows signs that inflationary pressures are easing. The latest quarterly CPI data showed inflation slowing to 2.8%, within the central bank’s target band for the first time in over two years.

At the same time, Australia’s unemployment rate ticked up to 4.3%, suggesting the labour market is cooling. Governor Michele Bullock emphasised that rate cuts are intended to support household budgets while avoiding a sharper economic slowdown.

Historically, rate cuts have encouraged borrowing and investment, but the RBA has signalled it will proceed cautiously to avoid re-igniting inflation in the housing sector.

Commonwealth Bank response

The Commonwealth Bank confirmed it will pass on the full 0.25% p.a. cut to its variable home loan rates, effective from 22 August 2025.

A spokesperson from the bank said the decision reflects their commitment to support customers during cost-of-living pressures. All changes will be visible in NetBank and the CommBank app from the effective date.

In addition to the headline 0.25% p.a. cut for variable rate loans, the Commonwealth Bank has clarified how the change will affect different customer groups.

- Owner-occupiers paying principal and interest will see standard variable rates drop from 6.39% to 6.14%.

- Investors with interest-only loans will experience a reduction from 6.84% to 6.59%.

- Low-deposit borrowers under the bank’s special LVR tiers will also see proportional cuts.

These changes will apply automatically from 22 August 2025, and borrowers can check updated rates through NetBank, the CommBank app, or by contacting their lender.

How much can borrowers save?

If you have a $500,000 mortgage, this cut could save you around $74 a month based on RBA estimates. Over a year, that’s about $888 in extra breathing room.

However, Commonwealth Bank notes that actual savings can be much higher depending on loan terms. For example, a $500,000 mortgage could see annual savings of $2,884, and a $1 million loan could save up to $5,768 if customers keep repayments at current levels.

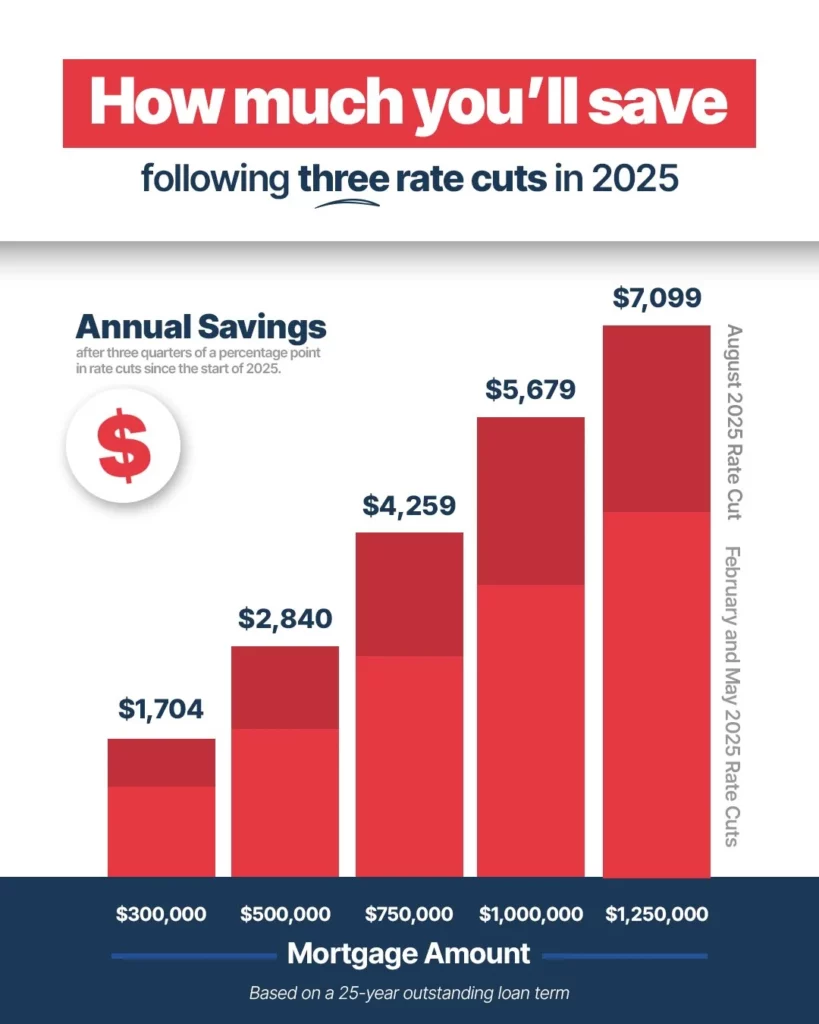

For everyday households, the cut can translate into significant yearly savings. Commonwealth Bank’s own modelling shows that after three RBA cuts in 2025, borrowers could be saving:

- $1,704 annually on a $300,000 loan

- $2,840 on a $500,000 loan

- $4,259 on a $750,000 loan

- $5,679 on a $1 million loan

- $7,099 on a $1.25 million loan

These figures assume a 25-year term and that repayments remain unchanged, meaning borrowers can use the extra funds to reduce the principal faster or cover other living expenses.

Tweet reactions from industry voices

“Passing on the full RBA cut is essential to help families manage cost of living pressures.”

“Rate cuts will flow through the economy gradually but are a welcome sign of easing conditions.”

“The RBA’s decision aligns with our forecasts for a gradual easing cycle into 2026.”

“This is the time for borrowers to reassess their mortgage strategies.”

These comments reflect both optimism and cautious planning as the cuts roll out.

Impact on fixed rate loans

Earlier this year, Commonwealth Bank also adjusted its fixed rate home loans, with reductions of up to 0.40% in May and a further 0.15% later that month. This brought some fixed rates down to 5.49% for owner-occupiers on a three-year term, improving affordability for those seeking repayment certainty.

Why this matters for the housing market

Lower borrowing costs can encourage more home buyers to enter the market, potentially increasing demand. However, the effect will depend on how long rates stay low and whether more cuts follow.

With housing affordability still a challenge in many regions, even small rate adjustments can change buyer sentiment.

Lower interest rates typically boost housing demand, especially among first-home buyers who find monthly repayments more manageable. However, with property prices already stabilising after last year’s correction, analysts are divided on whether the current cuts will trigger another sharp rise.

CoreLogic data shows that median home prices in Sydney and Melbourne have grown modestly in the past quarter, while Brisbane and Adelaide continue to record stronger gains. Economists warn that if rates continue to fall into 2026, affordability pressures could return despite the short-term relief.

What should homeowners do now?

If you have a variable loan with Commonwealth Bank:

- Check your updated interest rate after August 22.

- Decide whether to reduce your monthly repayments or keep them the same to pay off your loan faster.

- Review fixed rate offers, they may provide security if you expect rates to rise again.

- Consider refinancing if other lenders offer better deals.

If you are looking to buy, now may be a good time to compare mortgage products and factor in possible future rate cuts.

Borrowers can make the most of these rate cuts by taking a few proactive steps:

- Keep repayments at pre-cut levels to shorten your loan term and save thousands in interest.

- Review your offset account to ensure extra funds are reducing interest effectively.

- Compare competitor rates to see if switching could bring further savings.

- Consider splitting your loan between fixed and variable to balance flexibility with certainty.

Even small adjustments now can have a compounding benefit over the life of your loan, particularly if further cuts arrive later in 2025.

Economic outlook

Economists predict at least one more RBA cut by the end of 2025, possibly taking the cash rate down to 3.35 per cent. Some forecasts even suggest rates could drop below 3% by 2026 if inflation continues to cool.

If this happens, Commonwealth Bank is likely to adjust rates further, offering additional relief to borrowers.

Balancing relief and caution

While rate cuts are good news for borrowers, they also signal a slower economy. Reduced rates can lift borrowing, but they may also indicate softer job markets and weaker spending. For homeowners, the focus should be on using savings wisely and building financial buffers.

Conclusion

The Commonwealth Bank’s decision to cut home loan rates in line with the RBA’s latest move delivers meaningful relief to Australian mortgage holders. With inflation cooling and the economy adjusting, borrowers now have a chance to reassess their financial strategies.

As more cuts may be on the horizon, staying informed and proactive will be key. For many households, this step by the Commonwealth Bank is not just a number on paper, it’s a real improvement in day-to-day living costs.

Advertisement

FAQ’S

The Commonwealth Bank reduced home loan rates following the RBA’s latest cash rate cut to provide mortgage relief and support borrowers.

The reduced rates will apply from 22 August 2025 for eligible variable home loan customers.

Commonwealth Bank and Westpac have announced they will pass on the RBA’s latest rate cut in full to their variable home loan customers, effective 22 August 2025.

The Reserve Bank of Australia lowered the cash rate by 0.25 percentage points to stimulate the economy and reduce borrowing costs.

After the latest cut, the official cash rate set by the RBA stands at 3.75% per annum.

Australia’s 17% interest rate period occurred in the late 1980s and lasted for several months before gradually easing.

It means borrowing costs for banks, businesses, and individuals are lowered, encouraging spending and investment in the economy.

The Reserve Bank of Australia is wholly owned by the Australian Government and operates independently to set monetary policy.

The highest official cash rate in Australian history was 17.5% in January 1990.

Economists predict interest rates in 2025 will trend lower than early-year levels, with possible further cuts if inflation slows.

So far, the RBA has implemented three rate cuts in 2025 to support economic growth.

A rate cut reduces your mortgage repayments, potentially saving you hundreds of dollars annually depending on your loan size.

When the RBA holds rates, it usually means inflation is still a concern or the economy is performing strongly enough without stimulus.

Loan repayments and other borrowing costs decrease, while savings account interest rates often fall as well.

Disclaimer

This content is made for learning only. It is not meant to give financial advice. Always check the facts yourself. Financial decisions need detailed research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)