Did you know the Bank of Canada has raised interest rates more than ten times since 2022? These moves changed the way we borrow, save, and spend. One big forecast came from BMO (Bank of Montreal). They predicted the interest rate would fall to 2%. That number got people talking to homeowners, investors, and everyday shoppers like us.

So, what happened next? Did the rate go down to 2%, or did things take a different turn? In this article, we’ll explore BMO’s bold forecast and why it mattered. We’ll also look at how the Bank of Canada makes its rate decisions. Most importantly, we’ll see what this means for our money, our homes, and our future.

Advertisement

Let’s break it down in a simple way, no complex terms, just the real impact on us.

Background on Bank of Canada Interest Rates

The Bank of Canada sets an important number. It’s called the policy rate. This rate helps decide how much people pay to borrow money. When the Bank increases the rate, borrowing costs go up. People and businesses may borrow less. That means they spend less, which can help slow down rising prices.

But when the Bank lowers the rate, loans get cheaper. More people can afford to borrow. That leads to more spending and more investing. This helps the economy grow.

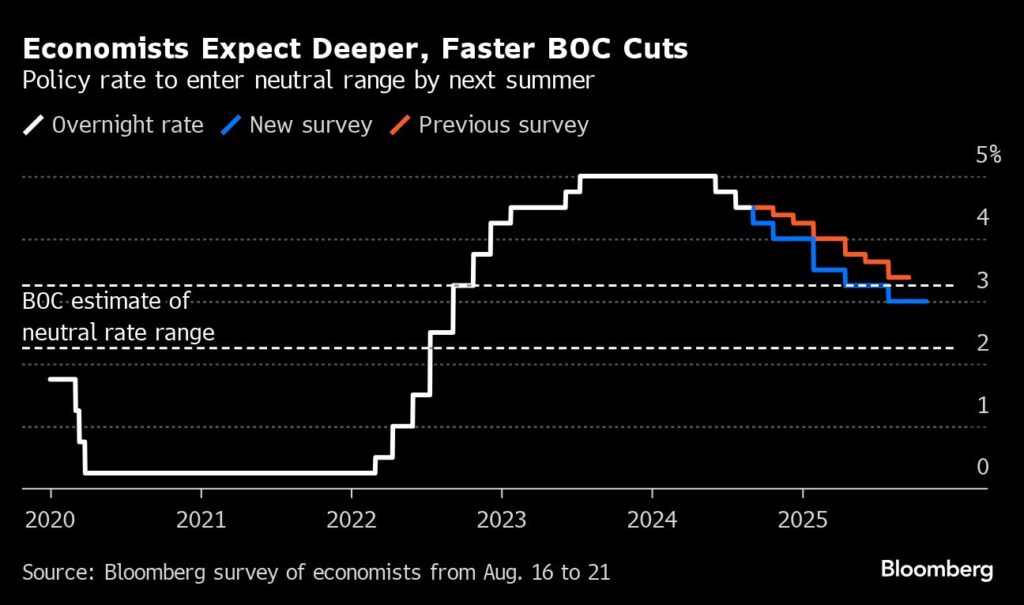

In recent years, the BoC increased rates to combat rising inflation. However, as inflation began to stabilize, the BoC started cutting rates to support economic growth.

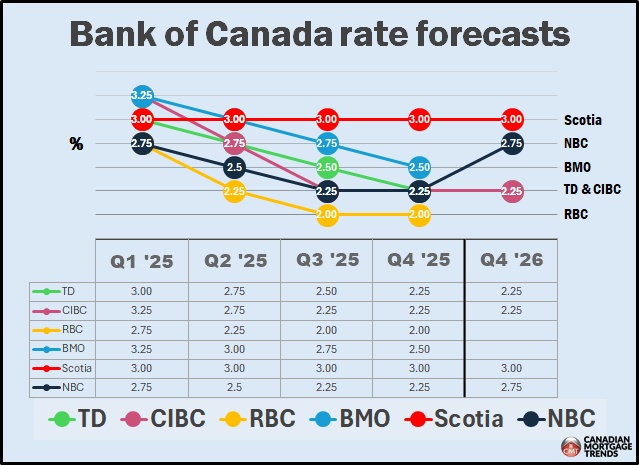

BMO’s Forecast and Rationale

In early 2025, BMO shared that the Bank of Canada could lower its interest rate to 2% by year-end. They believed trade troubles, especially with the U.S., might weaken Canada’s economy. If growth slowed down, the Bank might cut rates to boost activity.

BMO’s Chief Economist, Douglas Porter, said tariffs could hurt the economy more than they raise prices. Because of that, more rate cuts might be needed.

Actual Decisions by the Bank of Canada

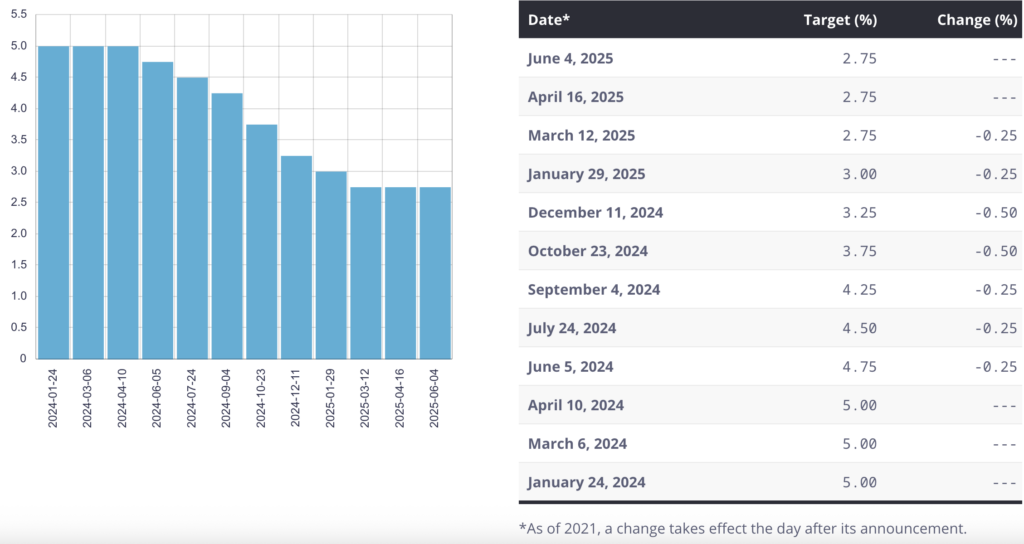

On June 4, 2025, the Bank of Canada decided to keep its policy rate unchanged at 2.75%. They did not change the cost of borrowing money. This decision came after a series of rate cuts totaling 2.25 percentage points since June 2024.

The BoC cited uncertainties related to U.S. trade policies and their potential impact on the Canadian economy as reasons for holding the rate steady.

Inflation has dipped to 1.7% in April, and core inflation remains above the BoC’s target range, reaching 3.15%. The BoC has indicated that it may consider further rate cuts if economic conditions deteriorate.

Economic Implications of a 2% Interest Rate

If the BoC lowers the policy rate to 2%, it would have several effects on the economy:

- Lower interest rates make loans and mortgages cheaper. This helps people and businesses borrow money more easily.

- When loans cost less, people may buy expensive things like houses or cars. This helps the economy grow.

- Cheaper mortgage rates can also help the housing market. More people may buy homes. This could raise home prices.

- Lower rates can also help businesses. They may borrow money to grow or hire more workers. This can create more jobs.

- But there’s also a downside. A lower rate might make the Canadian dollar weaker. That helps Canada sell goods to other countries. But it also makes imported goods cost more.

Market and Investor Reactions

People in the financial world watch the Bank of Canada very closely. After the June 4 update, the Canadian dollar went up a little. This showed that investors trusted the Bank’s careful choices.

But not everything is clear. Trade issues with the U.S. are still a problem. These worries make investors nervous. Some businesses are waiting before they spend or grow. They will analyze what happens next.

What This Means for the Future

BMO’s forecast of a 2% rate has not come true yet, but it could still happen if the economy gets weaker. The Bank of Canada said it may lower rates again if needed. That choice will depend on how the economy changes in the coming months.

For people making big money decisions, it’s smart to watch interest rate updates. If you plan to buy a home or invest, follow BoC news and key economic indicators. Lower rates might offer good chances, but it’s important to check your budget and plan wisely.

Bottom Line

BMO thinks the interest rate may drop to 2% by the end of 2025. This is because the economy is facing problems, especially from trade issues.

Right now, the Bank of Canada has stopped lowering rates. But what they do next will depend on how the economy changes. For us, it’s important to understand these updates. It helps us make smart money choices, even when things are uncertain.

Advertisement

Frequently Asked Questions (FAQs)

Experts think the Bank of Canada may lower its rate to around 2.25% by the end of 2025. This depends on inflation and how the economy performs.

Right now, the rate is 2.75%. Some forecasts suggest it could drop to 2.25% by late 2025 if the economy slows down.

Experts expect the rate to be around 2.25% to 2.50% in 2026. The main reasons will be how inflation and the economy grow.

The Bank of Canada’s next rate decision will be conducted on Wednesday, July 30, 2025, at 9:45 a.m. Eastern Time.

Disclaimer:

This content is only for learning. It is not financial advice. Always check facts and do your own research before making financial decisions.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)