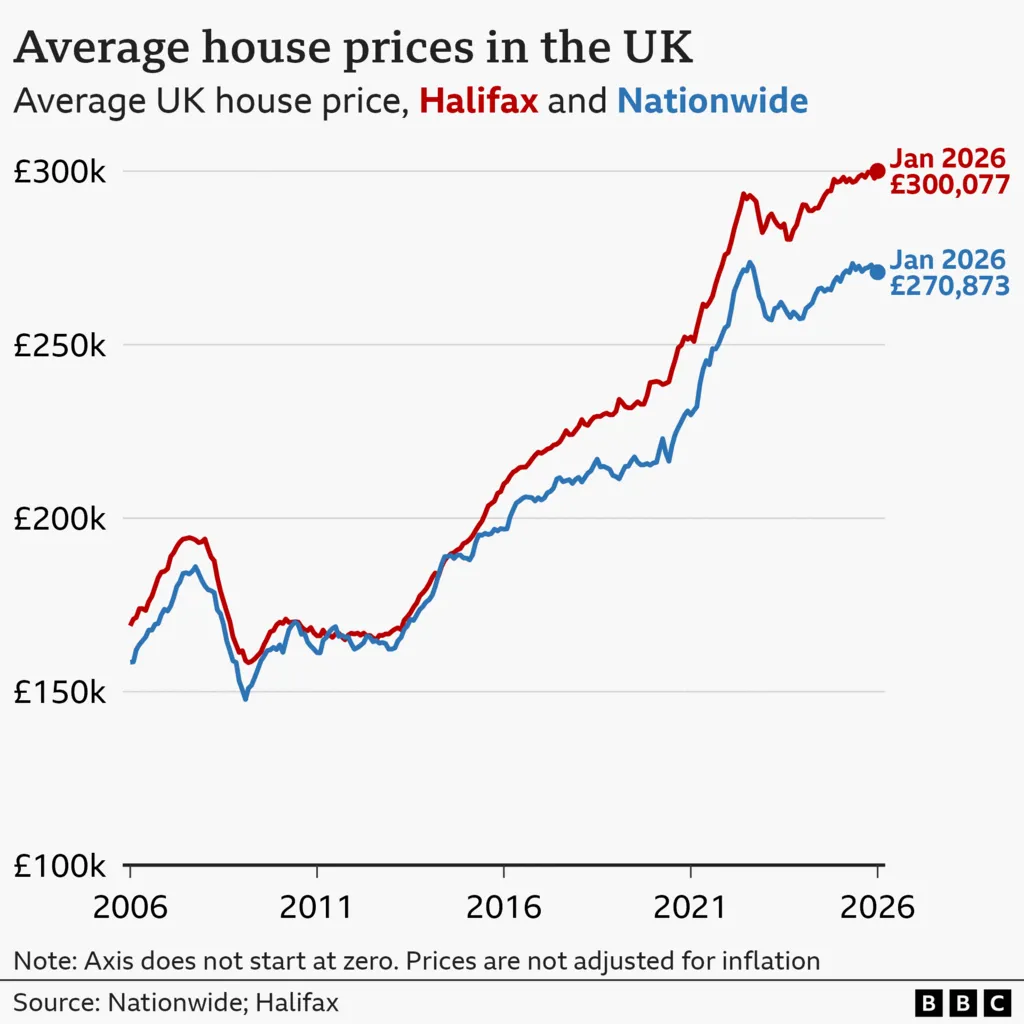

The UK house price milestone has finally arrived. In January 2026, the average property value reached £300,077, marking the first time prices crossed £300,000 nationwide. Monthly growth stood at 0.7%, while annual gains edged up to 1.0%, signaling a steady but restrained recovery. This shift reflects easing borrowing costs, resilient demand, and gradual wage improvements supporting affordability.

Even so, regional disparities and long-term affordability pressures remain central risks for buyers and investors. Understanding what pushed the UK house price to this historic level helps frame expectations for housing demand, lending trends, and property-linked investment opportunities in 2026.

Market Momentum Behind the £300,000 Breakthrough

Rate Cuts, Wages, and Demand Stability

The latest UK house price rise follows improving macro conditions. January’s 0.7% monthly gain reversed December’s 0.5% decline, confirming renewed demand at the start of 2026. Annual growth also strengthened to 1.0%, reflecting cautious but positive momentum. Analysts link this stability to falling mortgage rates, wage growth outpacing property inflation since late 2022, and gradually improving credit availability. These factors collectively support transaction activity without triggering rapid price inflation.

This shows the housing market is stabilizing rather than overheating. For investors, controlled growth often signals healthier long-term returns with lower correction risk.

Regional Divergence Shapes the UK House Price Outlook

Northern Strength vs Southern Moderation

Regional performance remains uneven across the UK house price landscape. Northern Ireland recorded 5.9% annual growth with average prices near £217,206, while Scotland followed at 5.4% and about £221,711. Meanwhile, England’s north-west leads English regions with 2.1% growth, highlighting stronger affordability-driven demand outside London.

Looking longer term, prices have risen only 5.7% over three years, far below the 19% surge seen between 2020 and 2023. This slower pace indicates structural cooling after the pandemic boom rather than market weakness.

For investors, regional divergence suggests a selective opportunity rather than broad nationwide upside.

Affordability Pressures Still Define the UK House Price Cycle

Growth Without Accessibility

Despite the record UK house price, affordability constraints persist. Economists note that stretched borrowing capacity and prior interest-rate shocks continue limiting buyer activity. Even with recent gains, policymakers and lenders view affordability as the main structural barrier to sustained expansion.

Encouragingly, wage growth has exceeded house-price inflation since late 2022, gradually improving real purchasing power. Mortgage deals below 4% are also re-emerging, suggesting incremental relief if inflation continues easing through 2026.

This balance between rising prices and improving affordability defines the current housing cycle.

Recent Updates on UK House Price Trends

- The average UK property value hit £300,077 in January 2026 after a 0.7% monthly rise.

- Annual growth increased to 1.0%, up from 0.4% the previous month.

- Prices climbed only 5.7% over the past three years, far below pandemic-era growth.

- Northern Ireland leads regional growth at 5.9%, followed by Scotland at 5.4%.

- Wage growth has exceeded house-price inflation since late 2022, improving affordability trends.

- Mortgage rates below 4% are gradually returning as inflation pressures ease.

Together, these signals confirm stabilization rather than speculative overheating in the housing market.

Market Sentiment and Social Signals

Broader sentiment around the UK house price milestone remains cautiously optimistic. Media coverage frames the £300,000 level as evidence of resilience supported by easing rates and steady demand.

Community discussions also highlight improving real wages and falling effective prices after inflation, suggesting selective buying opportunities for first-time purchasers and movers. For investors, sentiment indicates confidence in gradual appreciation rather than rapid upside.

Conclusion

Crossing the £300,000 threshold marks a symbolic turning point for the UK house price cycle. The data shows steady recovery driven by wage growth, easing borrowing costs, and resilient regional demand rather than speculative excess. At the same time, affordability constraints and uneven regional performance limit rapid expansion.

For investors and buyers, the key takeaway is moderation. Expect gradual price growth of roughly 1%-3% in 2026, selective regional opportunity, and improving financing conditions rather than a sharp boom. Long-term positioning in affordable, high-growth regions may therefore offer the most balanced risk-return outlook in the evolving UK housing market.

Frequently Asked Questions (FAQs)

The average UK property value reached £300,077 in January 2026 after a 0.7% monthly increase.

Annual UK house price growth stands at 1.0%, indicating modest but positive momentum entering 2026.

Northern Ireland leads with 5.9% annual growth, followed by Scotland at 5.4%.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)