Did you know that AMD just surprised Wall Street with better numbers than expected? In Q2 2025, the tech giant didn’t just meet goals it beat them, all thanks to strong demand for its AI chips. With the AI market booming, companies are racing to build faster, smarter systems. AMD is quickly catching up to big names like NVIDIA by focusing on high-performance AI hardware.

We’ve been watching the chip wars heat up, and AMD is making smart moves to stay in the game. Their new forecast for Q3 shows even more growth ahead especially in AI.

Advertisement

Let’s explore how AI strategy is working, what the AMD Q2 latest numbers show, and what this all means for investors and the future of tech.

AMD Q2 Results Breakdown

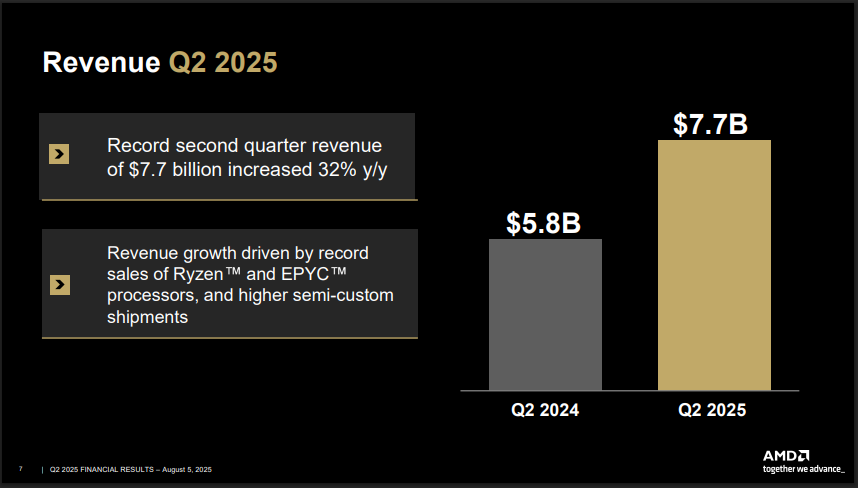

In Q2 2025, AMD posted revenue of about $7.7 billion, up roughly 32% year‑on‑year. That beat analysts’ estimates of around $7.43 billion. Adjusted earnings per share came in at $0.48, matching expectations.

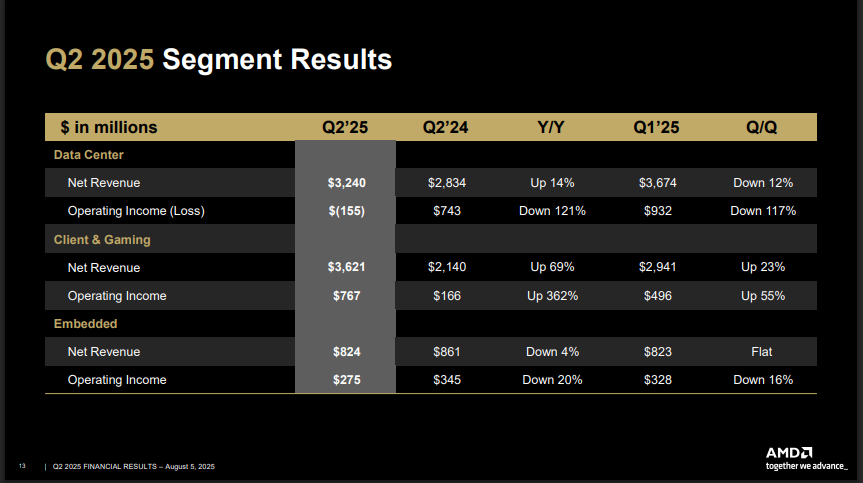

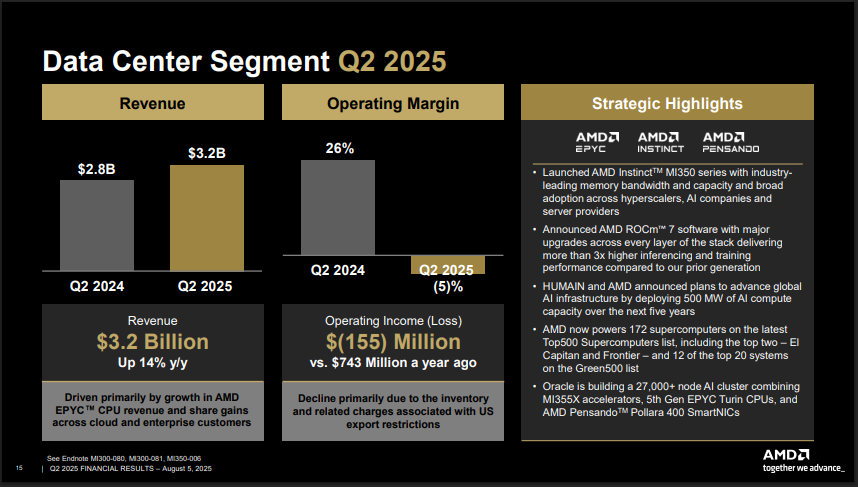

The Client segment generated $2.5 billion, up 67%, thanks to strong Zen 5 processor sales. Gaming revenue soared 73% to about $1.1 billion, driven by Radeon GPUs and custom console chips. The Data Center arm grew 14% to $3.2 billion, meeting expectations but trailing Nvidia’s 73% growth in the same space. Embedded segment fell slightly to $824 million, down 4% year‑on‑year.

Due to U.S. export limits on MI308 AI chips destined for China, AMD took an $800 million charge. This reduced its gross margin to 43%, down from a potential 54% without the hit. Net income still rose to $872 million, boosted by strong core sales, though operating results showed an operating loss of $155 million tied to the restrictions.

AI Segment: The Star Performer

While Data Center growth was modest, AI chips remain the clear highlight. AMD is rolling out its Instinct MI350 series, including MI350X and MI355 accelerators. These chips begin volume production in June, ahead of schedule.

CEO Lisa Su emphasized strong demand from leading AI firms. She noted that seven of the top ten AI companies now use Instinct hardware. They see AMD as a viable and efficient alternative to Nvidia, especially for inference workloads.

Analysts believe that the new MI355 chips may offer performance nearly on par with Nvidia’s B200 chips but at a 30% lower average price. That gap gives AMD a competitive edge as hyperscalers seek cost-effective AI solutions.

Q3 Outlook and Guidance

AMD forecasts Q3 revenue around $8.7 billion, plus or minus $300 million. That beats the analyst consensus of $8.28-8.3 billion. Gross margin guidance sits near 54%, assuming no further China-related charges.

This outlook excludes any MI308 chip sales to China due to pending U.S. license approvals. Once licenses clear, AMD expects to recover much of the previous losses in coming quarters. Su said inventory issues linked to Chinese shipments will take “a couple of quarters to run through”.

AMD vs NVIDIA & Intel in AI Race

Nvidia still dominates AI training workloads. Its Data Center segment grew 73% in the same period that AMD grew only 14%. But AMD is gaining traction in AI inference, where price, power, and energy efficiency matter more.

AMD is closing the gap with lower pricing and emerging performance from the MI350 lineup. Analysts believe its MI355 accelerators give significant leverage to steal deals from larger players. Meanwhile, Intel continues to lag in server AI chips, giving AMD more runway to grow.

Investor Reaction and Stock Performance

Even though AMD beat on revenue and set a strong Q3 outlook, shares fell 3-6% after hours. Many investors felt expectations were already high, and the missing China sales raised concerns.

Overall, AMD’s stock had gained over 40% year‑to‑date, well ahead of the semiconductor index’s ~12% rise. Traders noted that the earnings rally may need fresh catalysts to continue, especially stock moves tied to China export clarity and MI355 ramp.

Strategic Moves & Partnerships

In the earnings call, Su highlighted AMD’s end-to-end strategy. This includes recent acquisitions like ZT Systems, which adds rack-scale AI server technology to AMD’s portfolio.

AMD also continues investing in AI software and infrastructure. It is building a broader software stack, integrating CPU and GPU offerings to support enterprise AI customers. The upcoming MI400 series is already drawing strong customer interest ahead of its rollout next year.

Risks & Challenges Ahead

Two major headwinds remain. First, the delay in MI308 chip exports to China is costly; AMD expects around $1.5 billion in lost revenue this year from the curbs.

Second, competition remains stiff. Nvidia’s dominance in AI infrastructure and Intel’s scale in server CPUs put pressure on AMD. Macroeconomic risks like inflation and geopolitical tension could also impact demand.

Execution risk is real too AMD must ramp MI350 and later MI400 series quickly while managing inventory clean‑up and meeting AI unit economics targets.

AMD Q2 Results: Final Words

We see AMD positioning itself as a serious AI infrastructure player. While it still trails Nvidia in scale, its new MI350 series and competitive pricing offer hope. The Q3 forecast of roughly $8.7 billion shows growing confidence, even without China‑bound AI sales.

Going forward, the chips to watch are the MI355 and MI400 series. And investors will want updates on China licensing and customer adoption. If AMD can deliver on both, we expect sustained momentum. This AI push could reshape AMD’s growth path in 2025 and beyond.

Advertisement

Frequently Asked Questions (FAQs)

Meyka AI gives AMD a “B+” grade for growth and market position, with a consensus price target around $155, suggesting a modest downside from current trading levels.

Many analysts rate AMD a “Buy,” but price targets suggest slight decline toward $155. Meyka sees solid fundamentals, though upside may be limited in short term.

According to Meyka’s long-term view, AMD could reach $200-$300 by 2029 if AI chips keep growing. But short-term odds are lower.

Disclaimer:

This is for information only, not financial advice. Always do your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)