The Altman Z-Score: Your Tool for Bankruptcy Prediction, formula, and applications

Predicting financial failure is more important than ever. Over 20,000 companies in the U.S. filed for bankruptcy in 2024 alone, a sharp rise from previous years. For investors, lenders, and business owners, the risk of collapse is real and growing. That’s where the Altman Z-Score comes in.

Created by Dr. Edward Altman in 1968, this simple yet powerful formula helps spot early signs of business failure before it’s too late. It uses five key financial ratios to calculate how likely a company is to go bankrupt. Backed by decades of research and used by analysts worldwide, the Z-Score still holds strong in 2025.

With AI-powered finance tools on the rise, the Z-Score is now being combined with machine learning to improve accuracy. Whether you’re an investor looking to avoid losses, a founder tracking your company’s health, or a student learning business basics, this tool can help you make smarter, safer choices.

The Altman Z‑Score: Your Bankruptcy Forecasting Tool or Technique in 2025

Origins & Evolution

In 1968, NYU Stern finance professor Edward Altman revealed the original Z‑Score model to predict bankruptcy in manufacturing firms using financial ratios. Since then, he introduced tailored versions: Z′ Score for private firms, Z″ Score for non-manufacturers, and an emerging-market version for economies like China and Turkey.

Today, these models serve investors and lenders in diverse markets—public, private, and international.

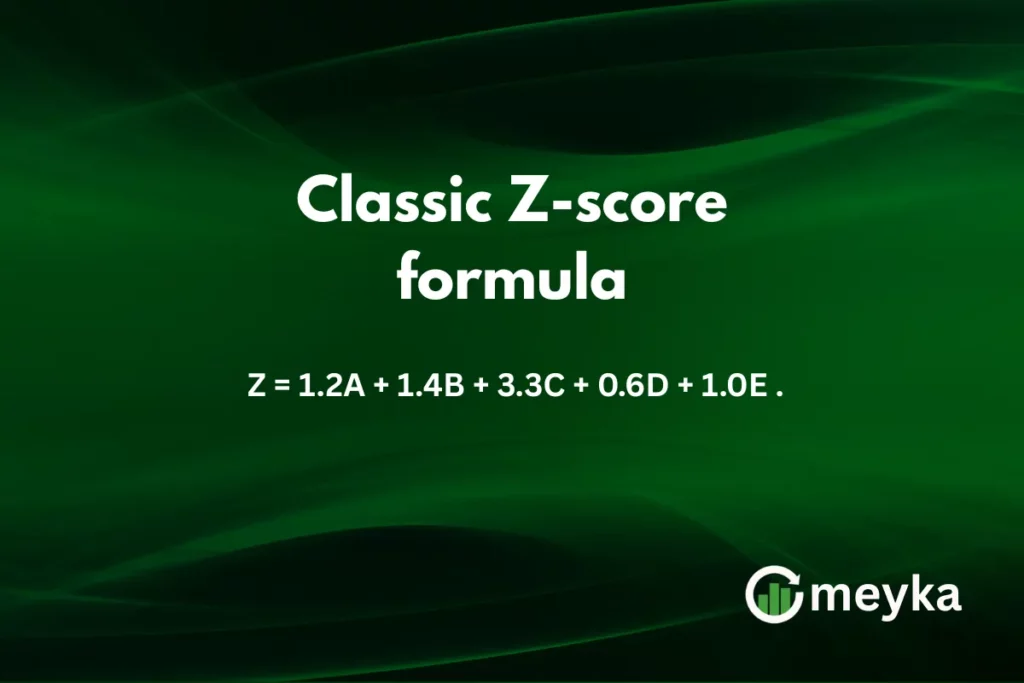

Formula Breakdown

- A = Working capital ÷ Total assets

- B = Retained earnings ÷ Total assets

- C = EBIT ÷ Total assets

- D = Marketplace value or worth of equity ÷ Total liabilities

- E = Sales ÷ Total assets

Thresholds: Z < 1.8 suggests distress, 1.8–3.0 is a “grey” area, >3.0 is safe. Altman recently highlighted that a score near 0, not 1.8, now signals danger.

Real-World Examples

C3.ai (AI), a public AI software firm with no debt and strong liquidity, shows a safe Z‑Score between 9 and 16 on different platforms:

- 9.35 (StockAnalysis.com)

- 15.99 (WallStreetNumbers.com)

- GuruFocus calculates 7.19 for fiscal year 2025. This places C3.ai in the “safe zone,” signaling strong financial health.

Conversely, firms with Z‑Scores near 0 or negative face a high risk, Altman estimated over an 80% chance of bankruptcy within two years.

Applications in Today’s Market

- Investors & Analysts use Z‑Scores to filter investments, avoiding low scores and favoring financially robust firms.

- Lenders & Fintechs layer Z‑Scores with AI tools, particularly where credit history is lacking.

- M&A & Distressed Deal Teams rely on Z‑Scores to evaluate acquisition or restructuring candidates.

AI & Machine Learning Integration

Modern risk models enhance the Z-score using machine learning:

- Random Forests and discriminant analysis applied to Turkish companies reached 95 %+ accuracy.

- AI-powered systems now combine financial ratios with market sentiment, offering real-time risk detection dashboards.

Market Impact & Benefits for Users

- Economic Relevance: Amid global inflation, rising interest rates, and recession worries, the Z‑Score gives a clear risk signal.

- Fintech Adoption: Platforms like Finbox, Koyfin, and Simply Wall Street include Z‑Score analysis.

- Global Reach: Its use has spread to Asia, Africa, and emerging markets where credit data is weak.

User Advantages:

- Reduced Investment Risk: Spot risky investments early.

- Smart Decision-Making: For lenders, founders, and analysts.

- Financial Literacy: Teaches how key balance-sheet ratios reflect viability.

- Startup Insight: Helps small firms track their financial health.

Strengths & Limitations

Pros:

- Easy to compute and interpret

- Powerful historical reliability, up to 95 percent within 1 year of bankruptcy.

Cons:

- Leans on accounting figures, might miss a hidden threat

- Not valid for financial institutions.

- Some modern models, like Ohlson O-Score and hazard models, may perform better.

Best Practices & Tips

- Update regularly, use quarterly reports, especially during economic changes.

- Blend Qualitative Checks, review leadership quality, and market position.

- Use Smoothed Metrics, rolling averages prevent seasonal distortions.

- Add an AI component, identify anomalies in real-time.

Conclusion & Outlook

The Altman Z‑Score remains a strong tool or technique into 2025. Simple enough for quick checks and flexible enough to integrate with AI, it’s ideal for investors, fintech platforms, SMEs, and analysts. By combining timeless financial insight with modern data analytics, the Z‑Score offers a sharp lens for spotting early warning signs, helping users make smarter, more informed decisions.

FAQS

The Altman Z-Score is utilized to forecast the likelihood of a firm’s bankruptcy by identifying financial ratios related to growth, leverage, liquidity, activity, and solvency.

The Altman Z-Score credit rating tool evaluates a company’s financial health. It estimates bankruptcy risk using a formula based on key financial ratios from balance sheet and income statement data.

An Altman’s Z-score of 3.5 indicates that the firm is in the safe zone, meaning it has a lower risk of bankruptcy and is financially healthy or strong.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)