Alphabet Inc. is the parent company of Google. Most people know that. But what many miss is how quietly powerful this company really is.

Every day, billions of people use Google Search, YouTube, and Android. These tools feel like part of our daily routine, and that’s exactly the point. Alphabet has built a system that works silently in the background while creating massive value.

While flashy tech stocks get all the attention, Alphabet keeps growing. It’s not just surviving, it’s leading. Alphabet is more than just an ad company with strong cash flow, bold bets on the future, and a growing cloud business.

Let’s explore why Alphabet might be the hidden compounder you’re overlooking. We’ll highlight the facts and show you why long-term investors should take a closer look.

What Makes a Stock a Compounder?

We define a compounder as a firm that grows steadily. It earns strong profit margins. It reinvests cash well, builds a deep moat, so competitors struggle to catch up. When a company checks these boxes, it can deliver outsized wealth over time. Alphabet quietly matches this profile. Many overlook its steady strength under the shiny headlines.

Alphabet’s Core Engine: Google Search & Ads

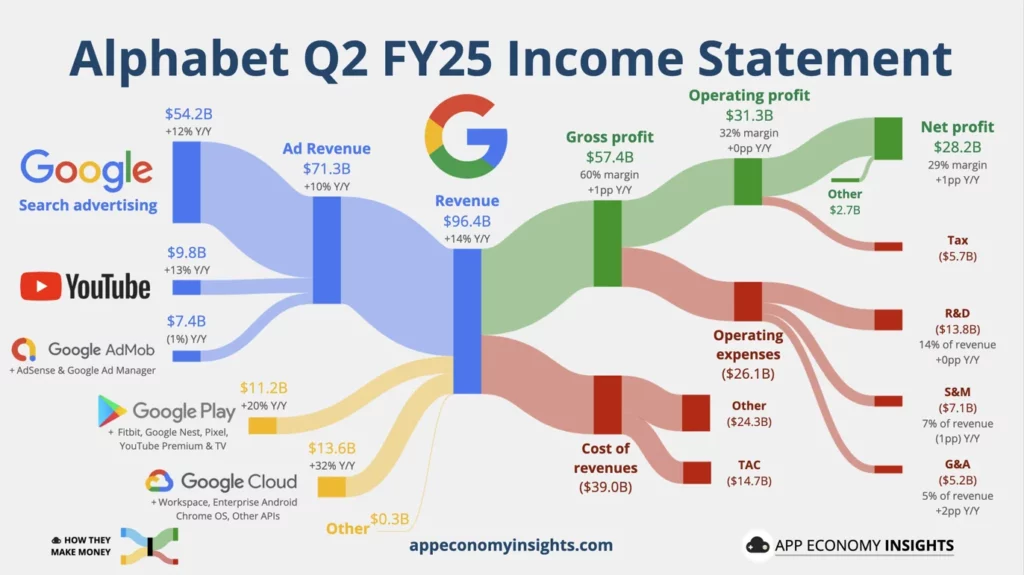

Google Search remains the bread and butter. It brings in the bulk of ad revenue. In Q2 2025, Search ads generated about $54 billion, up over 12 percent year over year. That shows real dominance.

This reliable ad cash fuels everything else. Even when macro economies wobble, advertisers still pay for high‑intent traffic. That steady stream gives Alphabet freedom to invest, innovate, and grow without depending on market hype.

The Underappreciated Segments

YouTube

YouTube is more than a video site. In Q2, ad sales grew 13 percent to nearly $9.8 billion. YouTube Shorts, its short‑form video platform, now earns similar or better revenue per watch hour than full‑length YouTube in the U.S.. Subscriptions like Premium and Music are also growing fast and reached over 270 million paid users in early 2025.

Google Cloud

Cloud is no longer just an investment area. It earned $13.6 billion in Q2, up 32 percent year over year, and is now profitable. Its enterprise footprint is expanding via AI Infrastructure and generative AI tools. More big deals, often over $250 million, are closing every quarter.

These segments together diversify Alphabet’s revenue and reduce reliance on Search ads alone.

The Moonshots: Bets on the Future

Alphabet keeps investing in long‑shot ventures within “Other Bets.”

Waymo, its autonomous vehicle arm, has rolled out real rides in cities like Phoenix, LA, SF, and plans expansion to Miami, Austin, and Atlanta by 2026. It already logged over 4 million driverless rides by the end of 2024.

Other experiments include DeepMind (AI research) and Verily (healthcare). These areas lose money now Other Bets segment lost ~$1.2 billion in Q2, but they offer potential optionality that could multiply value down the road.

Financial Strength & Capital Discipline

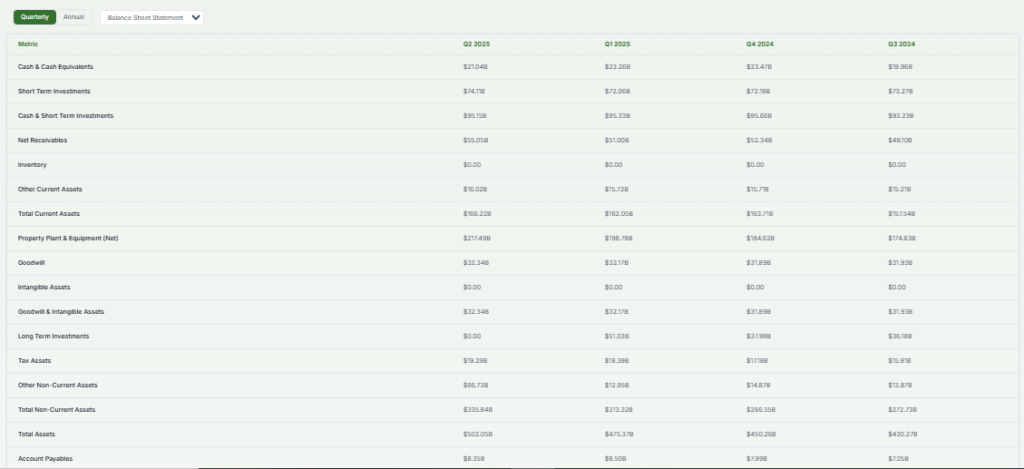

Alphabet’s balance sheet is rock solid. As of June 30, 2025, it held nearly $95 billion in cash and short‑term investments. It had modest long‑term debt of about $23.6 billion after issuing $12.5 billion in bonds earlier in the year.

On the return side, the company continues to share wealth with investors. In Q2, it increased its quarterly dividend by 5 percent and bought back billions of dollars in stock, supported by its strong liquidity.

Still, Free Cash Flow fell from over $17 billion to $5.3 billion this quarter. That drop stems from a massive surge in capital spending: ~$22 billion in Q2 alone, and guidance now points to $85 billion in CapEx for full‑year 2025, up from prior estimates. Most of this is for AI infrastructure expansion.

So, short‑term cash flow is under pressure. But we believe the reinvestment into AI infrastructure and global data centers is deliberate. If returns follow, these investments could pay off handsomely over the long haul.

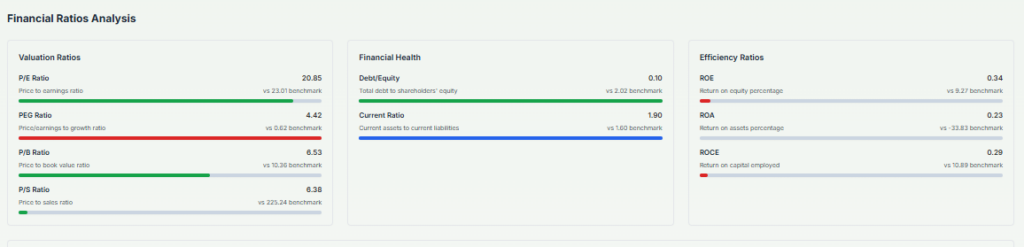

Valuation: Hiding in Plain Sight

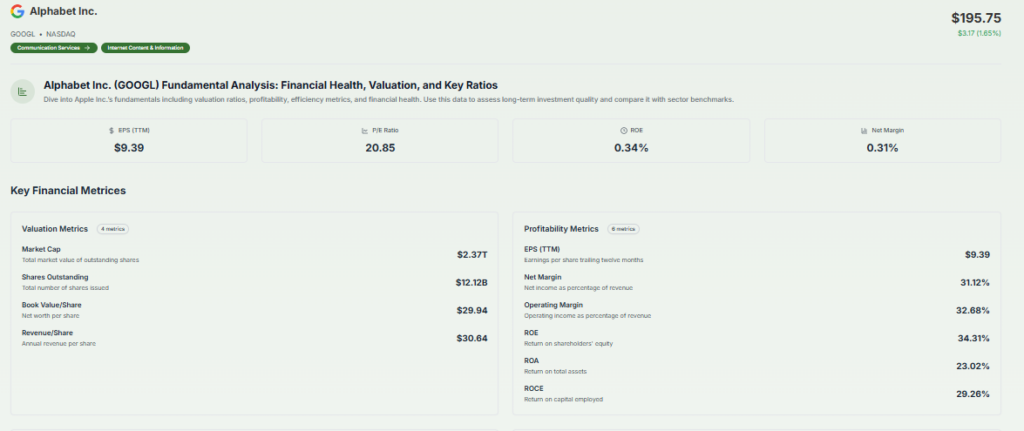

Alphabet still trades at modest multiples compared to fellow “Magnificent Seven” tech peers. Forward P/E sits around 25×, and P/FCF around 20×, not cheap, but reasonable given growth prospects.

Its mix of businesses, Search, Cloud, YouTube, and AI tools creates a sum‑of‑the‑parts value that the market may not fully price yet. Many believe the Company is undervalued by nearly 25-30 percent intrinsic discount compared to its net worth.

And it still yields tangible returns: growing buybacks, dividends, and steady margins (operating margin held at 32.4 percent this quarter) support shareholder value even during capex ramp‑ups.

Risks and Challenges

Several real threats could impact Alphabet’s trajectory:

- Regulatory scrutiny. Alphabet faces antitrust actions in the U.S. and EU. These could result in fines, structural changes, or limits on default services, any of which might disrupt the business model.

- Search disruption. A new wave of AI search tools like ChatGPT or Perplexity challenge the old ad‑driven model. While Google itself rolled out AI Mode and Search Generative Experience (SGE), longer-term slippage in search usage habits could diminish ad yields.

- Capital burn risk. Rising CapEx digs into cash flow. If future returns don’t justify the spending, margins may weaken and valuations adjust downward.

- Execution risk. Moonshots like Waymo or DeepMind may not scale as hoped, or could carry hidden costs and delays. Not every bet pays off.

Why Long‑Term Investors Should Pay Attention?

We still think Alphabet fits the bill of a hidden compounder. It grows at a steady pace. It reinvests heavily in AI, builds moats across Search, Cloud, YouTube, and its own AI stack.

Its capital strength lets it fund growth without dilution. Even as Free Cash Flow dips now, we see the spending as a bet, not a drain. If AI, Cloud, Shorts, and Other Bets start paying off, future cash flow will rise faster. That could drive a re‑rating.

Investors who can stay patient may find Alphabet offers both stability and long‑term optionality. It may not be the flashiest stock on the block, but it quietly builds value over time.

Final Words

Alphabet is more than an ad company. It’s a multi‑pillar tech platform with Search, YouTube, Cloud, AI tools, and moonshot innovation. Recent results show solid growth: revenue up 14 percent, net income up 19 percent, and strong YouTube and Cloud momentum. All while Alphabet doubles down on AI investment with record CapEx.

Yes, near‑term margins feel pressure. Yes, regulatory and competitive risks loom. But history shows Alphabet has managed big transitions well from Android to Cloud to AI.

Today, we believe it still qualifies as a hidden compounder: well-funded, wisely diversified, and building for the future. Patients who hold steady may be rewarded as its AI bets mature.

Frequently Asked Questions (FAQs)

Alphabet owns Google, YouTube, Android, Google Cloud, Fitbit, DeepMind, Waymo, Verily, and more. These companies work in ads, video, phones, cloud, AI, health, and self-driving cars.

Alphabet is underperforming due to high spending on AI, lower ad growth, and rising competition. Also, new rules and lawsuits are putting pressure on its business choices.

Disclaimer:

This is for information only, not financial advice. Always do your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)