Airbnb’s stock took a hit recently, and here’s why it matters. In early August 2025, the company shared its outlook for the second half of the year. The forecast? Slower growth than investors were hoping for. As soon as this news dropped, the Airbnb share price started to fall.

Now, if you’ve ever booked a stay through Airbnb, you know how big it is in the travel world. But even big names face bumps in the road. The slowdown isn’t just about numbers. It’s about changing travel habits, rising costs, and what people expect from vacations today.

Let’s break down what caused the drop, what Airbnb said, and how this could affect investors, travelers, and the whole short-term rental industry.

Airbnb’s Q2 2025 Performance Snapshot

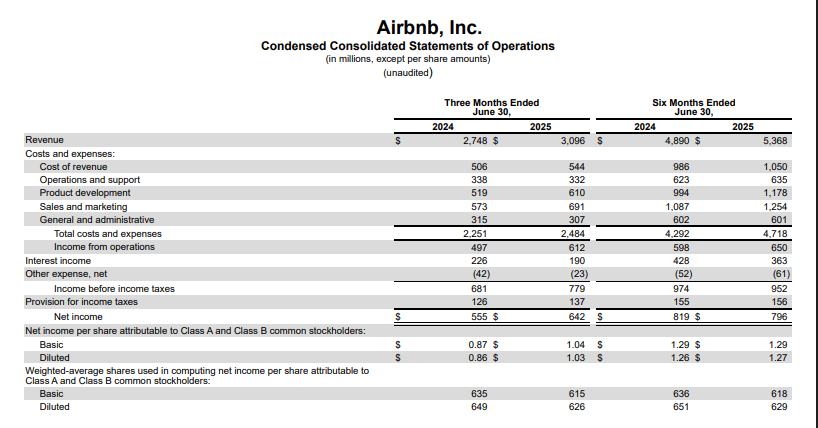

We saw Airbnb deliver strong results in the second quarter of 2025. Revenue climbed to $3.1 billion, a 13% jump from the same period last year. Net income rose 16% to $642 million, a healthy 21% margin. Adjusted EBITDA grew 17% to $1 billion, reaching a 34% margin. Cash flow was strong at $1 billion, and they bought back $1 billion of stock. Looking ahead, Airbnb is launching a new $6 billion share repurchase program.

Slower Growth Forecast for H2 2025

Even with a great second quarter, we’re seeing weaker projections for the rest of 2025. Airbnb warned of slower growth ahead. This caution comes from tough comparisons with last year’s high booking volumes, especially in Asia and Latin America, where bookings surged about 20%.

The company pegs its Q3 revenue at $4.02 to $4.1 billion. That sits around analyst expectations, but it hints at cooling momentum.

Investor Reaction and Stock Movement

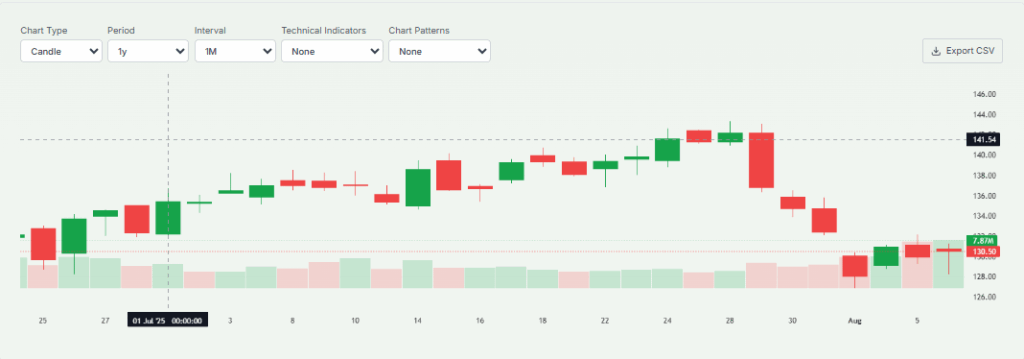

Investors reacted fast. Shares dropped roughly 6% after hours when the slower-growth warning hit. Despite the Q2 beat, this drop shows how sensitive the market remains to future guidance.

Not long before, analysts had downgraded Airbnb to “sell” due to weak summer travel in both the U.S. and Europe. The new target of $106 per share suggests a 17% drop from then.

Airbnb Share: Factors Behind the Forecast

Several factors are at play. First, comparisons are tough. Asia and Latin America had explosive growth last year, making it hard to match.

Second, economic uncertainties weigh on travel demand. Consumers are cautious, especially amid rising costs and softer sentiment.

Third, tariffs and new policy pressures are squeezing margins. Airbnb expects EBITDA margins to shrink in Q3 due to investments and advocacy costs.

Finally, regulations in many big cities limit short-term rentals. Listing growth in major markets has shrunk from 25% of total listings in 2017 to around 8% now.

Airbnb’s Strategic Response

To tackle these headwinds, Airbnb is pushing new ideas. The company is rolling out services like local tours, cleaners, spa treatments, and even celebrity events. These are part of a push to deepen its platform beyond lodging.

They also plan to spend $200-$250 million in 2025 on these new ventures. It’s their play to become more than a booking site.

Airbnb is also investing in local politics. They’re backing regulation-friendly policies and candidates to ease restrictive rental laws.

Industry Comparison & Competitor Outlook

We see a mixed picture across travel stocks. Analysts remain upbeat overall, naming travel a sector above GDP growth. Still, they see stronger positions for companies like Booking Holdings, which offer broader services and AI-driven features.

Airbnb, by comparison, faces a slower growth path. Its strategy relies on diversification and new services to remain competitive.

What Does This Mean for Investors?

So, what do we make of this? The strong Q2 shows Airbnb still has solid fundamentals. But the growth warns signals a rough patch ahead.

If you’re a long-term investor, you might view the stock dip as a buying opportunity. Price targets today range from about $134 to $165, suggesting upside for those who believe in Airbnb’s new strategy.

Short term, though, investors should brace for volatility. Weak summer travel and economic pressure could continue to weigh.

Wrap Up

We’ve seen strong Q2 numbers, but cautious outlooks for H2. Airbnb faces headwinds like tough comps, tougher rules, and slow demand. Its new services and buybacks offer hope, but results may take time.

This feels like a moment to watch closely. For patient investors, Airbnb’s next chapter might hold promise. But near-term turbulence is likely.

Frequently Asked Questions (FAQs)

As of August 2025, Airbnb expects slower growth for H2. Meyka shows ABNB trading near $130.5, with limited upside. It’s rated “Neutral,” signaling caution.

According to Meyka, ABNB is trading around $130.5 and showing limited short-term momentum. Most analyst targets sit between $130 and $165, depending on growth recovery.

The stock dropped due to slower growth forecasts, soft summer bookings, and tighter city rules. Investors worry about future demand and rising costs.

Airbnb’s market cap is around $85 billion based on its current price ($130.5). Meyka shows trading volume and neutral sentiment, reflecting cautious investor behavior.

Disclaimer:

This is for information only, not financial advice. Always do your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)